Vail Resorts posted its fiscal third-quarter 2025 financials yesterday, reporting a solid financial performance despite a dip in skier visits across its North American resorts. The company’s mix of mountain businesses and careful spending helped offset the drop in visitors, as the ski industry adjusts to new trends in travel and recreation. The results come just a week after a leadership transition, with Rob Katz returning to the CEO role, replacing Kirsten Lynch.

“Through the 2024/2025 North American ski season, guest satisfaction scores across our destination mountain resorts and regional ski areas were strong and consistent with prior year, excluding Park City Mountain.”

– Rob Katz

Key Mountain Segment Results for Q3 2025

- Lift revenue climbed 3.3% year-over-year to $770.3 million, driven by a 5.5% increase in pass product revenue, largely due to higher pass pricing for the 2024/2025 North American ski season. Non-pass lift revenue remained flat, with gains from the newly acquired Crans-Montana resort in Switzerland offset by fewer non-pass visits at North American destinations.

- Ski school revenue dipped slightly by 0.6% to $160.2 million, reflecting decreased skier visitation, partially balanced by higher lesson prices and incremental revenue from Crans-Montana.

- Dining revenue edged up 1.4% to $111.0 million, with growth from Crans-Montana helping offset lower guest numbers elsewhere.

- Retail and rental revenue fell 7.8% to $113.7 million, driven by a 10.1% drop in retail sales at on-mountain locations and a 5.5% decrease in rental income, both linked to reduced skier traffic.

- Operating expenses increased 3.4% to $19.2 million, attributed to the addition of Crans-Montana and higher general and administrative costs, partially offset by lower variable expenses tied to decreased revenue.

- Mountain segment EBITDA decreased by 0.5% to $647.7 million, factoring in $3.9 million in one-time expenses for the company’s ongoing resource efficiency transformation plan and $0.1 million in acquisition costs.

Season Trends and Outlook

- Total skier visits at North American resorts declined 3% year-to-date, but advance commitment strategies and strong guest spending helped support revenue growth.

- Season pass revenue rose 4% year-to-date, highlighting continued loyalty among core passholders.

- Early season pass sales for 2025/2026 show a 1% decrease in units but a 2% increase in dollar sales, reflecting higher pricing and resilient demand.

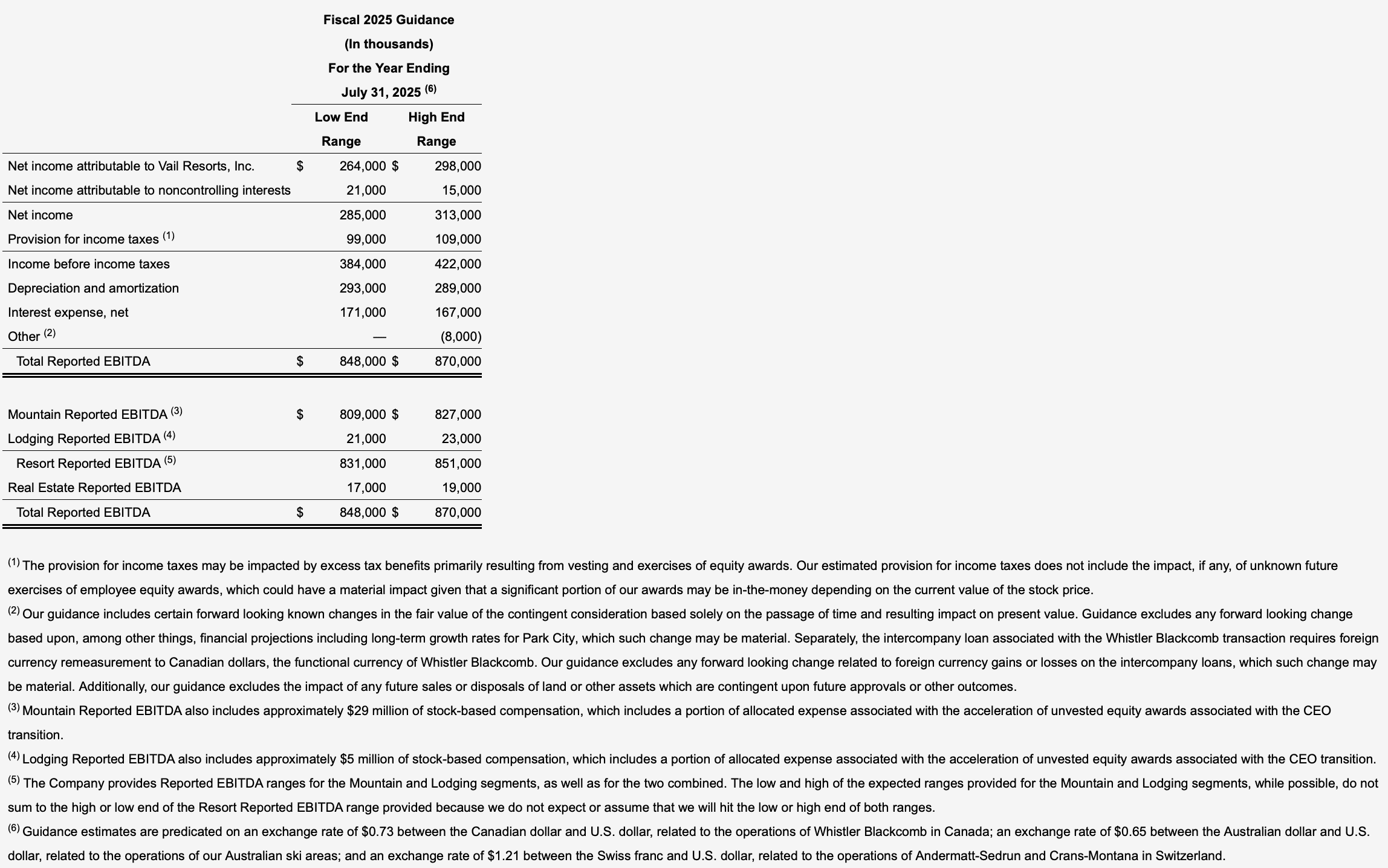

- Vail Resorts updated its full-year guidance, now projecting net income between $264 million and $298 million, and Resort Reported EBITDA between $831 million and $851 million, inclusive of one-time costs and foreign exchange impacts.

- The company declared a quarterly dividend of $2.22 per share and expanded its share repurchase authorization, signaling confidence in its long-term strategy.

For the ski community, the numbers reflect a season of adaptation, where pricing, passholder loyalty, and strategic acquisitions shape the mountain experience as much as snowfall and skier turnout. The leadership change at the top signals a new chapter as Rob Katz returns to guide Vail Resorts through the evolving landscape.

Full press release below:

BROOMFIELD, Colo., June 5, 2025 /PRNewswire/ — Vail Resorts, Inc. (NYSE: MTN) today reported results for the third quarter of fiscal 2025 ended April 30, 2025, updated fiscal 2025 guidance, and provided early season pass sales results.

Highlights

- Net income attributable to Vail Resorts, Inc. was $392.8 million for the third quarter of fiscal 2025 compared to $362.0 million in the same period in the prior year.

- Resort Reported EBITDA was $647.7 million for the third quarter of fiscal 2025, which included $4.2 million of one-time costs related to the previously announced two-year resource efficiency transformation plan and $0.1 million of acquisition and integration related expenses. In the same period in the prior year, Resort Reported EBITDA was $654.4 million, which included $1.3 million of acquisition related expenses.

- The Company updated its fiscal 2025 guidance and is now expecting net income attributable to Vail Resorts, Inc. to be between $264 million and $298 million and Resort Reported EBITDA to be between $831 million and $851 million, which includes an estimated $15 million of one-time costs in support of the Company’s resource efficiency transformation plan, an estimated $9 million in one-time costs related to the Company’s previously announced Chief Executive Officer (“CEO”) transition, and an estimated $1 million of acquisition and integration related expenses specific to Crans-Montana. In addition, compared to the original fiscal 2025 guidance, the updated guidance includes an estimated $7 million Resort Reported EBITDA impact from declines in foreign exchange rates.

- Pass product sales through May 27, 2025 for the upcoming 2025/2026 North American ski season decreased approximately 1% in units and increased approximately 2% in sales dollars as compared to the prior year period through May 28, 2024. Pass product sales are adjusted to eliminate the impact of changes in foreign currency exchange rates by applying current U.S. dollar exchange rates to both current period and prior period sales for Whistler Blackcomb.

- The Company’s Board of Directors declared a quarterly cash dividend of $2.22 per share of Vail Resorts’ common stock that will be payable on July 9, 2025 to shareholders of record as of June 24, 2025, and the Company repurchased approximately 0.2 million shares during the quarter at an average price of approximately $161 per share for a total of $30 million. The Board of Directors increased the Company’s authorization for share repurchases by 1.5 million shares to approximately 2.8 million shares.

Commenting on the Company’s fiscal 2025 third quarter results, Rob Katz, Chief Executive Officer, said, “Results in the quarter reflect the stability provided by our season pass program as Resort net revenue, excluding Crans-Montana, remained consistent with prior year even as visitation declined 7%. In March and April, destination visitation among pre-committed passholder guests improved as expected. However, visitation from uncommitted lift ticket guests was below expectations. Ancillary spend per destination guest visit was strong across our ski school and dining businesses throughout the quarter, while overall revenue in our ancillary businesses was impacted by the lower visitation.

“Our performance throughout the 2024/2025 North American ski season reflects the strength of our advance commitment strategy, strong destination guest spending, and the impact of our resource efficiency transformation plan. The Company achieved 3% growth in Resort Reported EBITDA year-to-date despite total skier visits declining 3% across our North American destination mountain resorts and regional ski areas from the beginning of the ski season through April 30, 2025. North American visitation reflects the benefit of improved conditions in the second quarter relative to the prior year, offset by the expected decline in visitation from selling fewer pass units this season. For the year-to-date period, Resort net revenue increased 3% driven by a 4% increase in season pass revenue and increased ancillary spend per guest across our ski school and dining businesses. Resort Reported EBITDA year-to-date also reflects strong cost discipline, including savings from the resource efficiency transformation plan. The Company’s full year Resort Reported EBITDA growth is partially offset by $15 million of expected increased costs from company-wide performance-based management incentive plan expense that was not earned in the prior year, of which $12 million has been incurred through the fiscal third quarter, and $6 million expected unfavorable EBITDA impact from changes in foreign exchange rates, of which $4 million has been incurred through the fiscal third quarter. Overall, the results demonstrate the strength and resilience of the Company’s business model, supported by its expansive resort network and loyal guest base, even as the Company’s western North American destination resorts experienced a decline in visitation, with outsized impacts from a decline in lift ticket guests.

“Through the 2024/2025 North American ski season, guest satisfaction scores across our destination mountain resorts and regional ski areas were strong and consistent with prior year, excluding Park City Mountain. As a result of the investments we continue to make in our teams, the Company achieved record front line return rates and strong employee engagement scores across our mountain resorts during the winter season.”

Regarding the Company’s resource efficiency transformation plan, Katz said, “Vail Resorts is on track to achieve its two-year resource efficiency transformation plan, which was announced in September 2024. The two-year resource efficiency transformation plan is designed to improve organizational effectiveness and scale for operating leverage as the Company grows. Through the three pillars of scaled operations, global shared services, and expanded workforce management, the Company expects $100 million in annualized cost efficiencies by the end of its 2026 fiscal year. The Company now expects to deliver approximately $35 million of efficiencies before one-time operating expenses in fiscal year 2025, which includes $8 million of efficiencies the Company is accelerating into the current fiscal year from its original fiscal year 2026 plan. The Company remains on track to deliver $100 million in annualized cost efficiencies by the end of its fiscal year 2026.”

Operating Results

A more complete discussion of our operating results can be found within the Management’s Discussion and Analysis of Financial Condition and Results of Operations section of the Company’s Form 10-Q for the third fiscal quarter ended April 30, 2025, which was filed today with the Securities and Exchange Commission. The following are segment highlights:

Mountain Segment

- Total lift revenue increased $24.6 million, or 3.3%, compared to the same period in the prior year, to $770.3 million for the three months ended April 30, 2025, which was primarily due to an increase in pass product revenue of 5.5%, primarily driven by an increase in pass pricing for the 2024/2025 North American ski season. Non-pass product lift revenue was flat compared to the prior year and benefited from incremental non-pass revenue from Crans-Montana of $7.9 million and an increase in non-pass effective ticket price (“ETP”) (excluding Crans-Montana) of 6.6%, but was offset by decreased non-pass visitation at our North American resorts. Total non-pass ETP, including the impact of Crans-Montana, increased 1.3% compared to the prior year.

- Ski school revenue decreased $1.0 million, or 0.6%, driven by decreased skier visitation, partially offset by increased lesson pricing and incremental revenue from Crans-Montana.

- Dining revenue increased $1.5 million, or 1.4%, driven by incremental revenue from Crans-Montana, partially offset by decreased skier visitation.

- Retail/rental revenue decreased $9.6 million, or 7.8%, for which retail revenues decreased $6.1 million, or 10.1%, driven by lower sales at our on-mountain retail locations, and rental revenues decreased $3.5 million, or 5.5%, each driven by decreased skier visitation.

- Operating expense increased $19.2 million, or 3.4%, which was primarily attributable to incremental operating expenses from Crans-Montana and an increase in general and administrative expenses, partially offset by decreased variable expenses associated with decreased revenue upon which those expenses are based.

- Mountain Reported EBITDA decreased $3.2 million, or 0.5%, for the third quarter compared to the same period in the prior year, which includes $6.1 million of stock-based compensation expense for the three months ended April 30, 2025 compared to $5.4 million in the same period in the prior year. Mountain segment results also include one-time operating expenses attributable to our resource efficiency transformation plan of $3.9 million for the three months ended April 30, 2025, as well as acquisition and integration related expenses of $0.1 million and $1.3 million for the three months ended April 30, 2025 and 2024, respectively.

Lodging Segment

- Lodging segment net revenue (excluding payroll cost reimbursements) decreased $3.6 million, or 4.3%, to $78.7 million for the three months ended April 30, 2025 as compared to the same period in the prior year, primarily due to a decrease in revenue from managed condominium rooms as a result of a net reduction in our inventory of available managed condominium rooms proximate to our mountain resorts, as well as decreased demand, which was impacted by decreased destination skier visitation.

- Lodging Reported EBITDA decreased $3.5 million, or 22.1%, for the third quarter compared to the same period in the prior year, which includes $0.8 million of stock-based compensation expense for the three months ended April 30, 2025 compared to $0.7 million in the same period in the prior year. Lodging segment results also include one-time operating expenses attributable to our resource efficiency transformation plan of $0.3 million for the three months ended April 30, 2025.

Resort – Combination of Mountain and Lodging Segments

- Resort net revenue was $1,295.4 million for the three months ended April 30, 2025, an increase of $12.3 million as compared to Resort net revenue of $1,283.1 million for the same period in the prior year.

- Resort Reported EBITDA was $647.7 million for the three months ended April 30, 2025, a decrease of $6.6 million, or 1.0%, compared to the same period in the prior year, which includes one-time operating expenses attributable to our resource efficiency transformation plan of $4.2 million for the three months ended April 30, 2025, as well as $0.1 million of acquisition related expenses for the third quarter of fiscal 2025 compared to $1.3 million of acquisition related expenses for the third quarter of the prior year.

Total Performance

- Total net revenue increased $12.3 million, or 1.0%, to $1,295.6 million for the three months ended April 30, 2025 as compared to the same period in the prior year.

- Net income attributable to Vail Resorts, Inc. was $392.8 million, or $10.54 per diluted share, for the third quarter of fiscal 2025 compared to net income attributable to Vail Resorts, Inc. of $362.0 million, or $9.54 per diluted share, in the third quarter of the prior year.

Outlook

As a result of the lower than expected lift ticket visitation during the spring period announced on April 24, 2025, and one-time costs related to the CEO transition announced on May 27, 2025, the Company is updating its guidance for fiscal 2025. The Company now expects net income attributable to Vail Resorts, Inc. to be between $264 million and $298 million, and Resort Reported EBITDA for fiscal 2025 to be between $831 million and $851 million. The guidance reflects the lower than expected lift ticket visitation in the spring period that was partially mitigated by the Company’s focus on its resource efficiency transformation plan and strong cost discipline. The updated guidance now includes an estimated $9 millionin one-time costs related to the CEO transition, in addition to the estimated $15 million in one-time costs related to the multi-year resource efficiency transformation plan, and the estimated $1 million of acquisition and integration related expenses specific to Crans-Montana. Compared to the original fiscal 2025 guidance, the updated guidance includes an estimated $7 million impact from foreign exchange rates. At the midpoint, the guidance implies an estimated Resort EBITDA Margin for fiscal 2025 to be approximately 28.4% or 29.2% before one-time costs from the resource efficiency transformation plan and CEO transition.

The updated guidance also assumes (1) a continuation of the current economic environment and (2) normal weather conditions and operations throughout the Australian ski season and North America summer season. In addition, the updated guidance also reflects foreign currency exchange rate volatility as compared to the assumptions included in our original guidance provided on September 26, 2024. The updated guidance assumes foreign currency exchange rates as of June 4, 2025, including an exchange rate of $0.73 between the Canadian dollar and U.S. dollar related to the operations of Whistler Blackcomb in Canada, an exchange rate of $0.65 between the Australian dollar and U.S. dollar related to the operations of Perisher, Falls Creek and Hotham in Australia, and an exchange rate of $1.21 between the Swiss franc and U.S. dollar related to the operations of Andermatt-Sedrun and Crans Montana in Switzerland, and does not include any potential impacts related to future fluctuations in foreign currency exchange rates, which may be impacted by tariffs, trade disputes, or other factors.

The following table reflects the forecasted guidance range for the Company’s fiscal year ending July 31, 2025 for Total Reported EBITDA (after stock-based compensation expense) and reconciles net income attributable to Vail Resorts, Inc. guidance to such Total Reported EBITDA guidance.

Capital Structure and Allocation Update

As of April 30, 2025, the Company’s total liquidity as measured by total cash plus revolver availability and delayed draw term loan availability was approximately $1.6 billion. This includes $467 million of cash on hand, $508 million of U.S. revolver availability and $450 million of U.S. delayed draw term loan availability under the Vail Holdings Credit Agreement, and $215 million of revolver availability under the Whistler Credit Agreement. As of April 30, 2025, the Company’s Net Debt was 2.6 times its trailing twelve months Total Reported EBITDA.

Regarding the return of capital to shareholders, the Company declared a quarterly cash dividend on Vail Resorts’ common stock of $2.22 per share. The dividend will be payable on July 9, 2025 to shareholders of record as of June 24, 2025. In addition, the Company repurchased approximately 0.2 million shares during the quarter at an average price of approximately $161 per share for a total of $30 million. This amount brings the Company’s total fiscal year-to-date repurchases to $70 million for a total of 0.4 million shares. Additionally, the Board of Directors increased the Company’s authorization for share repurchases by 1.5 million shares to approximately 2.8 million shares.

Regarding calendar year 2025 capital expenditures, as previously announced, the Company expects its capital plan for calendar year 2025 to be approximately $198 million to $203 million in core capital, before $46 million of growth capital investments at its European resorts, comprised of $42 million at Andermatt-Sedrun and $4 million at Crans-Montana, and $6 million of real estate related capital projects to complete multi-year transformational investments at the key base area portals of Breckenridge Peak 8 and Keystone River Run, and planning investments to support the development of the West Lionshead area into a fourth base village at Vail Mountain. Including European growth capital investments and real estate related capital, the Company plans to invest approximately $249 million to $254 million in calendar year 2025. Key capital investments include the multi-year transformational investment plans at Park City Mountain, which includes the new Sunrise gondola out of the Canyons base area, along with beginner terrain improvements and restaurant upgrades, in addition to the investments at Andermatt-Sedrun and a six-pack lift at Perisher, new functionality for the My Epic App, more advanced AI capabilities for My Epic Assistant, and technology investments across the Company’s ancillary businesses.

Commenting on capital allocation, Katz said, “We remain committed to a disciplined and balanced approach as stewards of our shareholders’ capital. We continue to prioritize investments that enhance our guest and employee experience, provide high-return capital projects, and enable strategic acquisition opportunities. After these priorities, we focus on returning excess capital to shareholders. In the current environment, the Company looks to balance its approach between share repurchases and dividends. The current dividend level reflects the strong cash flow generation of the business with any future growth in the dividend dependent on a material increase in future cash flows and the Company also maintains an opportunistic approach to share repurchases based on the value of the shares.”

Season Pass Sales

Commenting on the Company’s season pass sales for the upcoming North American ski season, Katz said “Pass product sales through May 27, 2025 for the upcoming North American ski season decreased approximately 1% in units and increased approximately 2% in sales dollars as compared to the period in the prior year through May 28, 2024. Given elevated levels of macro-economic volatility that occurred throughout the spring selling period, it is currently unknown what, if any, impact that had on early pass decision making. Pass sales dollars are benefiting from the 7% price increase relative to the 2024/2025 season, partially offset by the mix impact from the growth of Epic Day Pass products. Pass product sales are adjusted to eliminate the impact of foreign currency by applying an exchange rate of $0.73 between the Canadian dollar and U.S. dollar in both periods for Whistler Blackcomb pass sales.

Katz continued, “The slight decline in units relative to the prior year season to date period was primarily driven by new pass holders and lower tenured renewing pass holders, which may reflect delayed decision making due to the macro-economic environment. Epic Day Pass products experienced strong unit growth driven by the strength in renewing pass holders. Overall renewing pass holder product net migration was relatively consistent with the prior three years.

“The majority of our pass selling season is ahead of us, and we believe the full year pass unit and sales dollar trends will be relatively stable with the spring results. We will provide more information about our pass sales results in our September 2025 earnings release.”

Regarding Epic Australia Pass sales, Katz commented, “Epic Australia Pass sales through May 28, 2025 increased approximately 20% in units and approximately 8% in sales dollars as compared to the period in the prior year through May 29, 2024. Epic Australia Pass sales are benefitting from the successful introduction of the Epic Australia 4-Day Pass, which is resonating with lower frequency skiers and riders in Australia.”

Earnings Conference Call

The Company will conduct a conference call today at 5:00 p.m. eastern time to discuss the financial results. The call will be webcast and can be accessed at www.vailresorts.com in the Investor Relations section, or dial (800) 245-3047 (U.S. and Canada) or +1 (203) 518-9765 (international). The conference ID is MTNQ325. A replay of the conference call will be available two hours following the conclusion of the conference call through June 12, 2025, at 11:59 p.m. eastern time. To access the replay, dial (800) 723-8184 (U.S. and Canada) or +1 (402) 220-2668 (international). The conference call will also be archived at www.vailresorts.com.